Debt can feel extremely heavy. Whether it’s credit cards, student loans, medical bills, or a car payment that stretches the budget every month, owing money has a way of stealing your peace. If you’ve ever laid awake at night doing mental math or felt that uneasiness in your stomach when a bill notification pops up, you’re not alone. As our family has grown, our expenses have too. We both decided to leave our high-paying careers so that we could prioritize starting a family (and prioritize time with them too) and be involved in our church. We have been through seasons of debt and it is debilitating. Sometimes we think, “will we be in debt forever?” And the answer is no! We are in control of our financial wellbeing and it is attainable.

Getting out of debt is possible and it doesn’t require extreme deprivation, multiple side hustles, or living on rice and beans forever. It’s about small, smart choices done consistently, paired with patience and grace for yourself along the way.

Here are practical, realistic tips to help you get out of debt and move toward financial freedom.

1. Start With the Full Picture

The first step is also the hardest: writing everything down.

List all of your debts:

- Credit cards

- Personal loans

- Student loans

- Medical bills

- Car loan payments

Include the balance, minimum payment, and interest rate for each one. Seeing the total can feel overwhelming, but having financial clarity will help you understand the full picture. Don’t judge yourself while doing this. Debt is common, and it doesn’t define your worth.

2. Create a Simple, Realistic Budget

A budget isn’t about restrictions. Again, it’s financial clarity to discover where your biggest debts are, where you can cut back, and how you can generate more income. I used to use Google Sheets to track our budget, but recently we discovered a free budgeting app (Budgetum) that we’ve enjoyed so far.

Instead of trying to track every penny, start with broad categories:

- Housing

- Utilities

- Food

- Clothes

- Transportation

- Debt payments

- Savings

- Fun/personal spending

Make sure your budget reflects your real life, not your “perfect” life. If you know you’ll spend money on coffee or eating out occasionally, plan for it. An unrealistic budget is one you’ll abandon.

Even finding an extra $50–$100 a month to put toward debt can make a big difference over time.

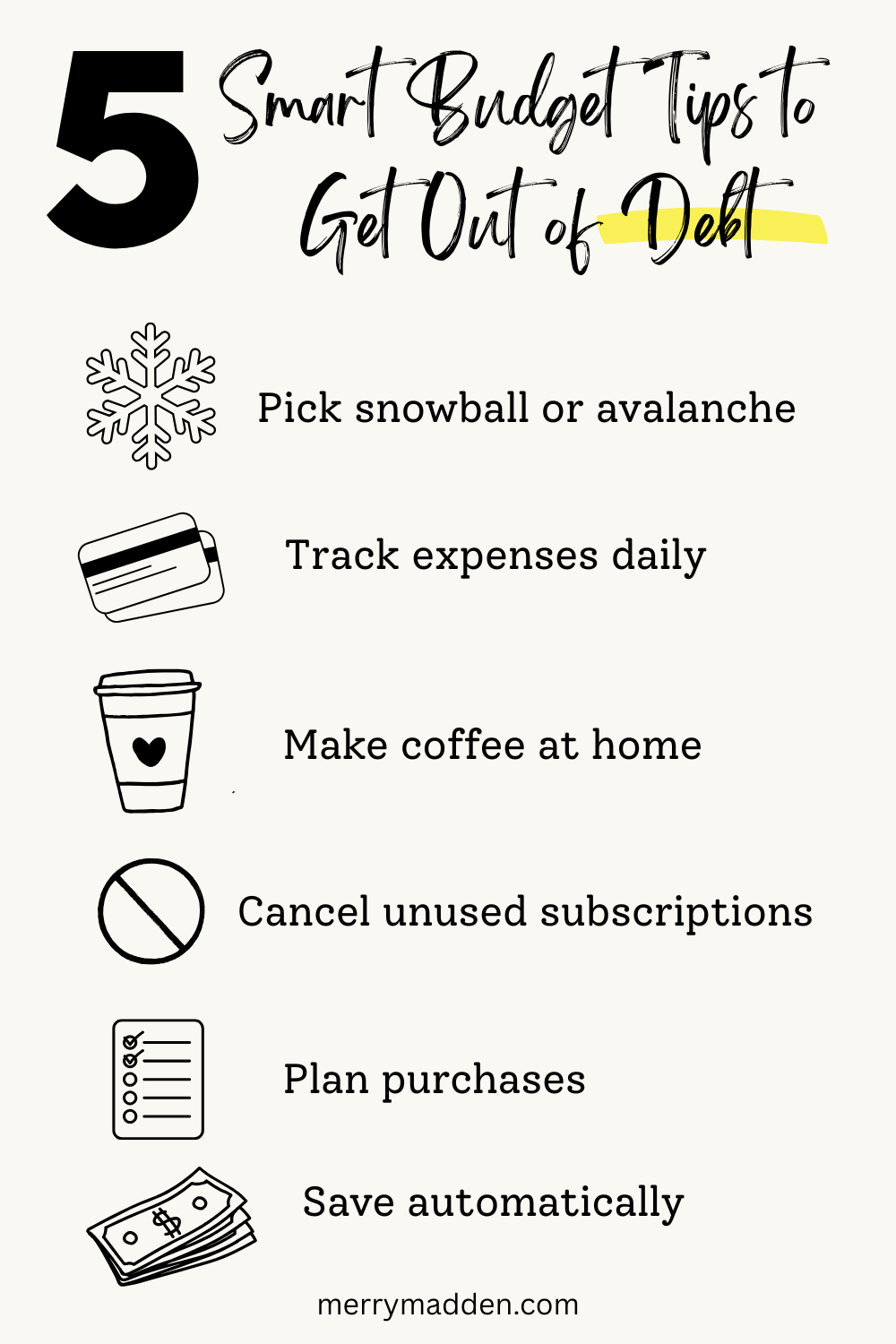

3. Choose a Debt Payoff Strategy

If you’ve ever watched/read about Dave Ramsey, you know he is a strong proponent of the debt snowball. I prefer the debt avalanche as it saves more money long term, and also I just don’t want a huge balance looming for very long. Choose what works best for you.

The Debt Snowball

- Pay off the smallest balance first

- Roll that payment into the next debt once it’s gone

This method builds momentum and confidence quickly.

The Debt Avalanche

- Pay off the highest interest rate first

- Saves more money on interest long-term

Both work. The “best” method is the one you’ll actually stick with.

4. Cut Expenses Without Making Life Miserable

You don’t need to cancel every joy in your life to get out of debt.

Start with easy wins:

- Make coffee at home (pause those Starbucks runs)

- Cancel unused subscriptions

- Negotiate internet or phone bills

- Meal plan to reduce food waste

- Avoid eating out

Look for temporary budget cuts rather than permanent deprivation. You can remind yourself, “This is for a season.”

5. Increase Income Where You Can

Sometimes the fastest way out of debt isn’t cutting more—it’s earning more.

Consider:

- Freelance or remote work

- Becoming an Amazon Affiliate

- Selling unused items around your home

- Babysitting, tutoring, or pet sitting

- Picking up extra hours temporarily

Even short-term extra income can help knock out a debt and free up cash flow.

6. Build a Small Emergency Fund

This step feels counterintuitive when you’re focused on debt, but it’s crucial.

In Dave Ramsey’s baby steps, the first step is to save $1,000 for your starter emergency fund. Aim for $500–$1,000 as a starter emergency fund. This prevents emergencies from going straight onto a credit card and undoing your progress.

7. Stop Using Credit While Paying It Off

If possible, pause credit card use while you’re paying down balances.

This might mean:

- Switching to cash or debit

- Removing saved cards from online shopping

- Auditing monthly automatic charges

It’s not forever, just long enough to break the cycle and gain control.

8. Track Progress and Celebrate Wins

Every paid-off balance matters—even small ones.

Track your progress visually:

- A debt payoff chart

- A spreadsheet

- Coloring in progress bars

Celebrate milestones without spending money:

- A special home-cooked meal

- A family movie night

- A quiet moment to acknowledge how far you’ve come

Progress fuels motivation.

9. Give Yourself Grace

You might overspend by one month. An unexpected expense might pop up. That doesn’t mean you’ve failed.

Debt freedom is built over time, not overnight. The key is getting back on track instead of quitting altogether.

10. Keep the Bigger Picture in Mind

Getting out of debt isn’t just about numbers—it’s about freedom.

Freedom to:

- Save for the future

- Give generously

- Reduce stress

- Be present with your family

- Make choices without fear

If faith is important to you, this can also be a season of learning to trust God with provision, wisdom, and patience. Small steps, done faithfully, add up.

Final Encouragement

You don’t need to have everything figured out today. You just need to take the next right step.

Whether that’s listing your debts, creating a simple budget, or paying an extra $25 toward a balance this month, it matters.

Debt doesn’t get the final word. With intention, consistency, and a little grace, freedom is closer than you think.

.webp)

.webp)